The Timing of Retirement Planning Returns

Are all returns created equally? Does it matter when you get positive vs. negative returns? When you are saving for a long-term goal like retirement, the likelihood of you having some years with negative returns is pretty high.

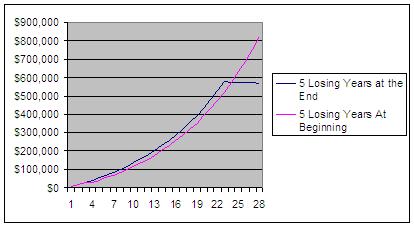

The reason I bring all this up is that I have been having an interesting conversation about retirement planning with a fellow on the Saving Advice website. The topic of the conversation was whether or not it matters if you get negative returns the first few years of a long-term goal or the last few years. Here are the assumptions made:

The goal is $1,000,000 thirty years from now. The assumed rate of return is 8%, which requires an annual contribution of $8,827. So, I took that information and plugged it into two different scenarios. The first scenario assumed that the portfolio lost 2% per year for the first 5 years and gained 8% thereafter. The second scenario assumed that the portfolio gained 8% per year for the first 25 years and then lost 2% per year for the last 5 years. I think the chart below makes it pretty clear:

Retirement Savings

Here's what the annual numbers look like:

So, from the looks of this, it is much better to have your losing years in the beginning rather than in the end.

The reason I bring all this up is that I have been having an interesting conversation about retirement planning with a fellow on the Saving Advice website. The topic of the conversation was whether or not it matters if you get negative returns the first few years of a long-term goal or the last few years. Here are the assumptions made:

The goal is $1,000,000 thirty years from now. The assumed rate of return is 8%, which requires an annual contribution of $8,827. So, I took that information and plugged it into two different scenarios. The first scenario assumed that the portfolio lost 2% per year for the first 5 years and gained 8% thereafter. The second scenario assumed that the portfolio gained 8% per year for the first 25 years and then lost 2% per year for the last 5 years. I think the chart below makes it pretty clear:

Retirement Savings

Here's what the annual numbers look like:

End of Account Account

Year ROR Value ROR Value

2 8% $9,533 -2% $8,650

3 8% $19,829 -2% $17,128

4 8% $30,948 -2% $25,436

5 8% $42,957 -2% $33,578

6 8% $55,927 -2% $41,556

7 8% $69,935 8% $54,414

8 8% $85,063 8% $68,300

9 8% $101,401 8% $83,298

10 8% $119,046 8% $99,495

11 8% $138,103 8% $116,987

12 8% $158,684 8% $135,879

13 8% $180,912 8% $156,283

14 8% $204,918 8% $178,319

15 8% $230,845 8% $202,117

16 8% $258,845 8% $227,820

17 8% $289,086 8% $255,579

18 8% $321,746 8% $285,558

19 8% $357,019 8% $317,936

20 8% $395,114 8% $352,904

21 8% $436,256 8% $390,670

22 8% $480,690 8% $431,456

23 8% $528,678 8% $475,506

24 8% $580,506 8% $523,080

25 -2% $577,546 8% $574,459

26 -2% $574,645 8% $629,949

27 -2% $571,803 8% $689,878

28 -2% $569,017 8% $754,602

29 -2% $566,287 8% $824,503

So, from the looks of this, it is much better to have your losing years in the beginning rather than in the end.

posted by JLP | 11:29 AM

| Email |

<< Home